The Hidden Cost of Kingmaking

Nobody talks about the companies that kingmaking kills.

If you’re a former employee, you have stock that’s either worthless or tied up in a company you’d rather not antagonize. If you’re a past investor, being open about what happened sounds like badmouthing a portfolio company. If you’re a founder who got rolled, you’re fundraising again and the last thing you need is a reputation for airing dirty laundry.

The incentives all point toward silence.

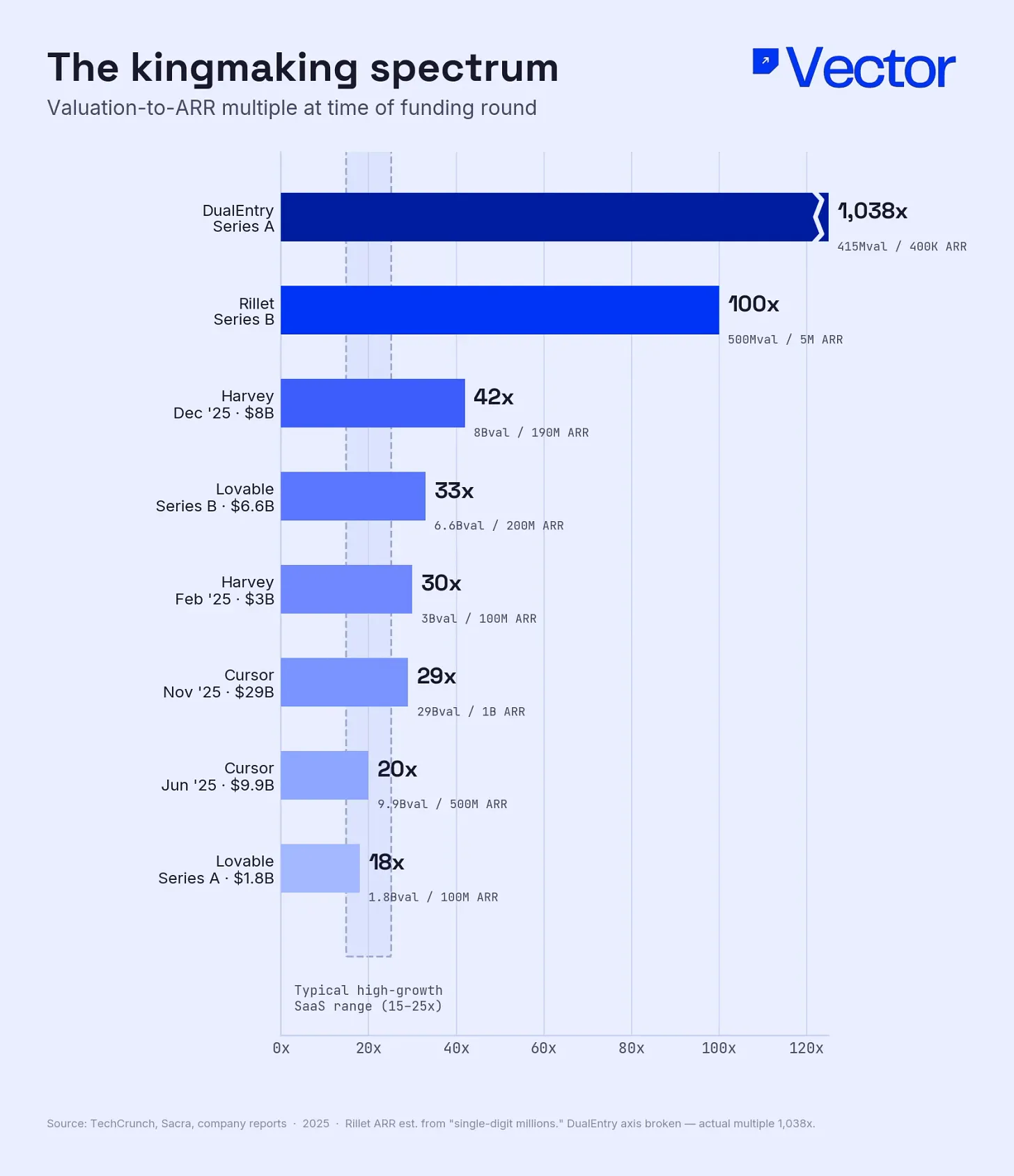

Vector published a great piece this week on kingmaking: the strategy of flooding a startup with so much capital that it appears dominant before it’s proved much of anything. It profiles the usual suspects, multi-billion dollar war chests, Series B rounds closing weeks after Series As with little new data in between.

What’s harder to see from the outside is what happens when it doesn’t work.

The article mentions Convoy and Bird as cautionary examples. Convoy raised $925 million, hit a $3.8 billion valuation, and sold for $16 million. Bird followed a similar arc into bankruptcy. But those are the visible failures.

Inside most of these companies, the story is taboo. The massive round gets announced. The narrative du jour gets amplified. The company hires aggressively. And then the GTM doesn’t work. The product isn’t sticky. Enterprise pilots don’t convert. The burn rate was set for a reality far ahead of progress.

These companies don’t die immediately. Many linger for years, but they’re already underwater.

The honest math of kingmaking is simple:

- If you nail GTM and the demand is real, capital is rocket fuel.

- If you don’t, you’ve just given yourself an extraordinarily expensive way to find out you were wrong.

Five years of runway sounds like eternity until you realize you need to quickly close the gap between progress and valuation. It’s like being helicoptered halfway up Mount Everest without training. The high feels great until pipeline stalls and layoffs become inevitable.

There’s a version of this that works beautifully. It requires overwhelming product-market fit, where capital is just oil on an existing fire. Harvey and Anysphere are examples of that, as was Uber in the last generation.

But those are the exceptions.

The dynamic that concerns me isn’t the investors, it’s the asymmetry facing founders.

The investor offering the term sheet may have seen this cycle fifty times. The founder accepting it has seen it zero, or maybe once or twice max.

Saying no to a massive round when your board, advisors, and employees are all telling you to take it requires a kind of restraint that’s unnatural. The best founders I’ve seen treat valuation as a tool, not a scoreboard. They raise what they need to prove the next thing, not what the market will give them.

That discipline is rare, especially when investors offer millions in secondaries to the founders.

Meanwhile, from the outside, this all looks like conviction. In reality, it’s often just capital deployed at scale.

When you’re sitting on a $15 billion fund, a $100 million check is portfolio allocation. You’re paid to invest, and you need large outcomes to move the needle. The strategy can work at the portfolio level even when many individual bets fail.

I’m not sure I’d behave differently in that position. In venture, your structure is your incentive.

But I do wonder what happens when everyone runs the same playbook at the same time, into the same categories, at the same stage, with the same narrative.

From where I sit, at a sub-$100 million seed fund where every check matters, it looks less like kingmaking and more like a very expensive way to find out who was right about product and GTM.

And by the time you find out, most of the capital is already gone.

The winners write the histories. The losers sign NDAs.

The Battle of La Roche-Derrien, 1347. The largest army ever assembled by Charles of Blois and he still lost.