Are VCs Paying More for Something Better, or Just Paying More?

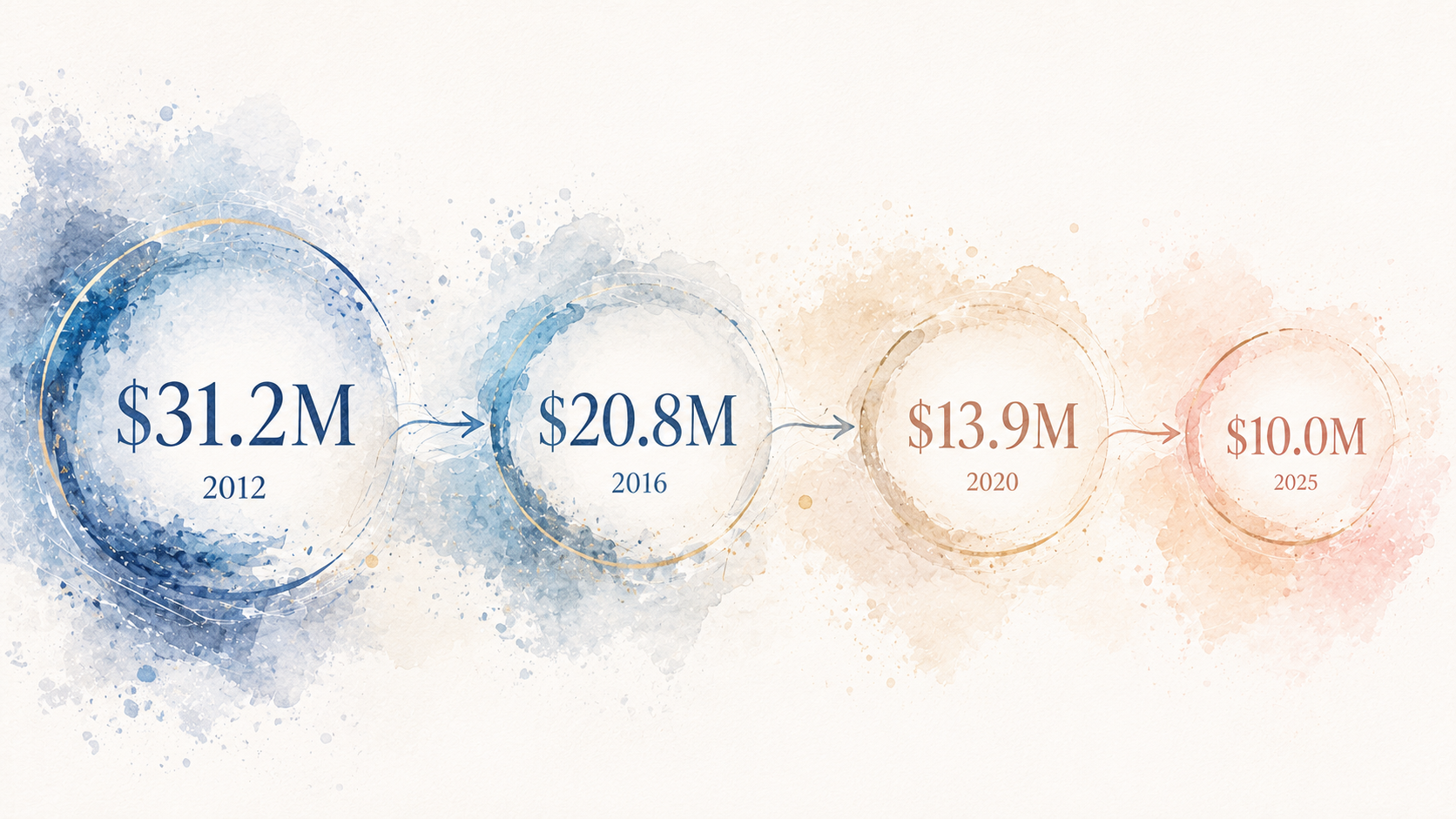

If you invested $500K in a startup in 2025 and it has a $1B exit, the value to your fund is two-thirds lower than the same exit from the same check written in 2012.

Some of our best-returning investments were sub-$1M checks. A few were under $500K. Several were in hardware companies. Companies that were hard to get funded at the time.

Those tiny investments produced some of our biggest multiples. But will that still be true for the investments we’re making today? We did some simple math:

A $500K check into an $8M post-money round in 2012 bought you 6.25% of a company. If that company eventually sold for $500M, your seed check returned over 30x (even after typical dilution). At a $5B outcome, you’re looking at north of 300x.

That same $500K check today? It buys you 2% of a company at a $25M post — roughly the median seed round right now. Same $500M exit, same dilution… and you’re looking at maybe 10x.

The check didn’t change. The exit didn’t change. But the return got cut by two-thirds.

People love to compare seed round inflation to CPI. Valuations are up ~2.5x since I started investing. CPI is up maybe 40% over the same period. “Seed inflation is outpacing regular inflation” is a known comment, but if you think of it in the context of how much more expensive (and harder) the business has gotten, it underscores how different things are.

Obviously it’s not an exact comparison. CPI measures a basket of goods that stays roughly constant. Milk is still milk. A seed round in 2026 is not the same product as a seed round in 2012. Today’s seed founder has often already raised $1-2M in pre-seed, has a shipped product, real metrics, sometimes meaningful revenue. Today’s seed is essentially 2015’s Series A.

So the question isn’t just “are we paying more?” It’s “are we paying more for something better, and does the math still work?”

Part of me thinks yes. More mature companies at seed means lower failure rates, more data to underwrite, less pure guesswork.

But our best returns didn’t come from certainty or the highest prices. They came from the weird ones. Uber back when getting into a stranger’s car was a bizarre idea. ShieldAI when defense tech was out of fashion. The TradeDesk after a dozen notable AdTech companies had crashed and burned. WHOOP when Will Ahmed was a student athlete. The hardware companies particularly stand out because they were often the hardest to fund.

The “market size” of those opportunities is a lot smaller these days, but they’re still there. We have to work harder to find them, but that’s where the alpha is.