Failure of Diversification: The Real Reason Seed Alpha Is So Elusive Right Now

I was chatting with some peers this week about where the “alpha” is in Seed investing right now. It feels elusive.

I have one theory: we’re not actually diversified. It’s investing 101, and yet we’re failing as an asset class.

In venture, the only diversification that reliably works is time diversification. But over the past few years everyone – GPs, LPs, Angels, and even Founders – ramped up deployment in the same cycle.

At the same time, the industry became highly correlated. Everyone is piling into the same sectors, the same themes, and often the same people and companies.

So even when people think they’re diversified, we really aren’t.

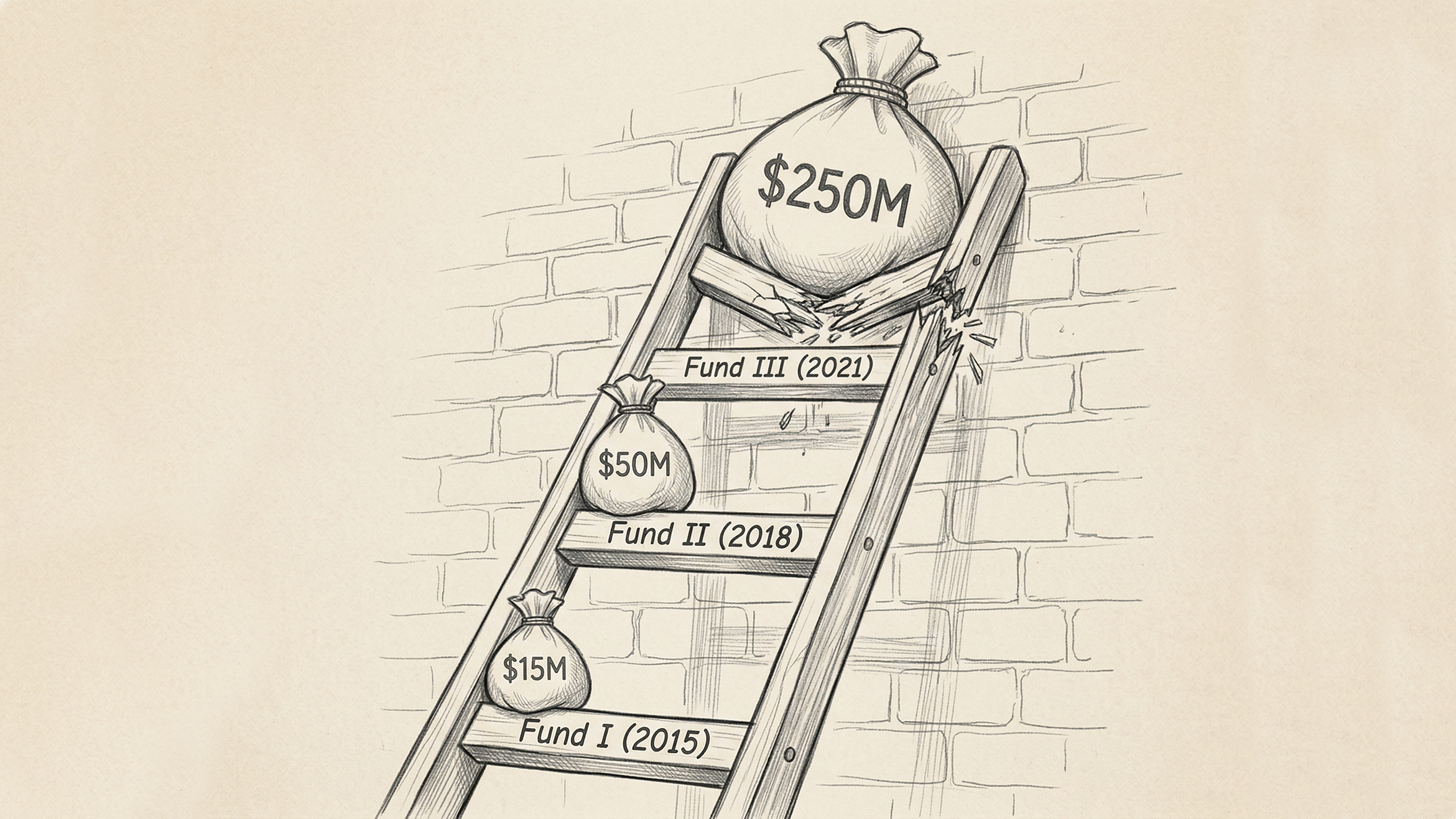

Look at the standard trajectory of a successful emerging manager:

- Fund I (2015): $15M

- Fund II (2018): $50M

- Fund III (2021): $250M

On paper, this VC has been investing for a decade.

In reality, nearly 80% of their deployed capital is locked in the peak-ZIRP 2021 vintage.

And because so many funds piled into the same sectors during that cycle, the portfolios often look eerily similar.

This is why at Founder Collective we’ve kept the fund size and pacing *relatively* consistent from fund to fund, year to year.

Angels and LPs made the exact same mistake.

During the bull run, they tried to diversify by deploying capital across 5 different micro-funds and syndicates in a single 18-month window.

Investing in 5 different managers in the same year isn’t diversification. It’s just buying the exact same overpriced macro risk 5 times over.

Cross-manager diversification does not solve vintage concentration – especially when many of those managers are investing in the same sectors and even the same deals.

Founders, this applies too.

If you raise massive amounts of capital, price your option pool, and anchor your exit expectations to a single market window, you are entirely exposed to vintage risk.

You aren’t building a resilient, multi-cycle business; your equity is tied heavily to the gravity of the year you raised.

So…

Alpha isn’t just about picking better companies or finding the hottest sector.

It is about structural discipline.

It is having the restraint to deploy equal dollars (and build steadily) across boring, down, and flat years not just when the market is screaming at you to go faster.

Easier said than done!