The Buy Window

The full spectrum of software is suddenly economic to attempt, but not all of it will be economic to own. That gap is probably the most important thing happening in software right now.

Every week I take calls with founders building things that would have been laughed at just a few years ago, not because the ideas were bad, but because they were uneconomical. Every product required multiple engineers, a product manager, and a designer. A two-person team can now ship what used to require a seed round and six engineers. In fact, we’re now seeing that pre-seed is typically pre-revenue with early pilot customers and companies raising seed rounds typically come with six-figure revenue.

While it’s now much easier to build, the rate limiting factor is still humans. We still need to prompt the model and massage the output, which is a real bottleneck people don’t often talk about. Yes, you can vibe code yourself software now, but it’s much harder to vibe code something used by many users, in deep domains or complex workflows. I was at a party over the weekend and a friend told me about how his wife used Claude Code to build herself a tool to manage her event planning business. Amazing use case for super powering her business, but I’m not sure it’s deep enough that I would pivot the solution into a new B2B SaaS startup.

Founders are building anything that can be built right now, which feels unlike anything I’ve seen. Everything is up for grabs and we all feel empowered. I don’t know about you, but vibe coding a dozen different apps in a dozen terminal tabs with Claude Code feels like the Limitless drug. The “why now” is just AI, which is surprisingly credible on the surface.

But I’m not convinced that every use case AI unlocks will actually accrue value to a company.

The logic goes: AI makes things possible, therefore startups will be built around those things, therefore those startups will be valuable. But that skips the step where the buyer has to choose not to just do it themselves.

Go try Claude Code. It is genuinely amazing. Even if you’ve never written a line of code and you have a weekend, you can vibe-code yourself a CRM, a dashboard, an internal tool, a niche workflow that solves your exact problem. The 80/20 is spectacular.

The last 20% is still annoying. Maintenance, edge cases, auth, permissions, integrations that break frequently. Building software as an individual, even with world-class tooling, still takes time, which is why commercial software exists in the first place.

So the question isn’t “can AI enable this?” The question is: will the person who could build this actually build this? And if not, what’s the right price?

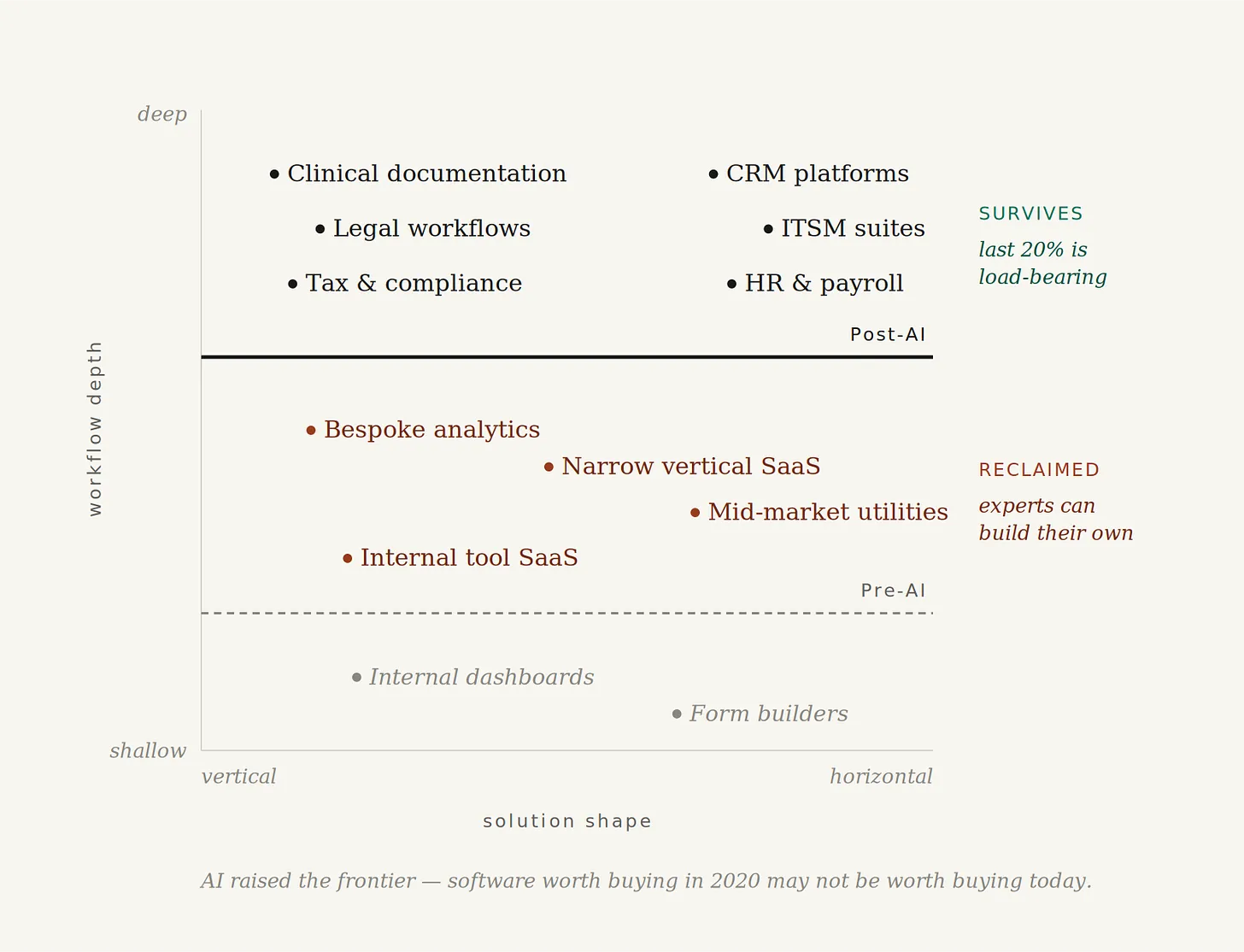

For a lot of workflows, the answer throughout the 2000s and 2010s was obviously no. That’s why Salesforce exists. You could build your own CRM, but you probably shouldn’t. The market for a good-enough generalized solution was enormous because the build cost was enormous and the generalization worked. Most companies needed roughly the same CRM.

Call that range of acceptable buy-versus-build decisions the Buy Window. It’s the band of workflows where the math tips toward buying rather than building, given the cost of the counterfactual. For two decades that window was wide and stable, and an entire generation of SaaS companies was built inside it.

AI is rapidly shrinking this window.

Take a concrete example. A custom PDF data extractor for a mid-market ops team used to be a $40K/year SaaS product with a few hundred customers. Today, an ops lead with Claude Code can ship a version that works for their specific documents in an afternoon. That product didn’t get worse. Its counterfactual collapsed. The Buy Window shifted away from it.

Compare that to clinical documentation software. A physician can’t vibe-code their way through HIPAA compliance, EHR integrations, payer-specific coding rules, and the audit trail requirements that make the product actually usable in a clinic. The last 20% is load-bearing, regulated, and domain-specific in a way that resists individual assembly. That’s still clearly inside the Buy Window, and probably will be for a long time.

Within that durable zone, two shapes matter: deep vertical plays like clinical documentation and legal workflows, which address smaller markets but produce sticky relationships, and deep horizontal plays like CRM and ITSM, which chase bigger markets with more competition. I suspect vertical is the more interesting hunting ground for the next wave, because horizontal has more incumbents with distribution, and because AI unlocks workflows in specialized verticals that weren’t worth addressing with software at all before.

The quadrant that’s collapsing is the one that used to be the bread and butter of mid-market SaaS: shallow-to-medium workflows sold to narrow audiences. If your product is something an operator could recreate in a weekend for their specific situation, the ceiling on your ACV just dropped. The alternative got radically cheaper, and ACVs will compress to reflect the new counterfactual.

Here’s the part I keep coming back to, and the part I suspect is going to be uncomfortable for a lot of founders.

Even for the companies that do build durable businesses in the right part of the Buy Window, ACVs will compress. It’s not just easier for your customers to build for themselves, but for other businesses to build a competitive product.

You paid Salesforce what you paid because the alternative was worse, engineering headcount, ops, infra, the whole stack. AI has slashed that alternative across the board. The internal build option isn’t free, but it’s meaningfully cheaper than it was. That’s a smaller wedge for the vendor to price into.

The best software businesses will still exist. They just need to be realistic and thoughtful about where the value accrues and plan accordingly.

You can already see this playing out in the public markets, which have been broadly unkind to software over the last year.

Part of it is AI exposure anxiety but I think the deeper thing is that the market is early and genuinely can’t distinguish yet between the software that’s still worth buying and the software whose buyer will eventually wake up and realize they don’t need to. The multiples are going to reflect that well before the revenue does, that’s usually how software repricing works.

The incumbents that can absorb compression tend to share features: capital-efficient cost structures, genuine distribution advantages, workflow depth that resists in-house replication. The ones that can’t have overbuilt sales orgs, thin product moats, revenue concentrated in the reclaimed zone and are going to have a hard time.

Not all is sad in the world of software businesses. There’s also a bull case, and it goes back to William Stanley Jevons, who noticed in 1865 that when steam engines became more efficient at using coal, England consumed dramatically more coal, not less. Efficiency made coal economical for a thousand new applications. The total market exploded even as the per-unit cost fell.

Apply that to software. If AI collapses the cost of building, we shouldn’t expect fewer software companies, we should expect vastly more. Problems that were never worth solving with software become solvable. Industries that couldn’t justify custom tooling suddenly can. Every niche vertical gets its own purpose-built workflow. The surface area of what software can economically address expands by an order of magnitude.

I think this is largely right. And I think it’s compatible with everything I just argued.

The two views only look contradictory if you conflate total market size with per-company ACV. Jevons argues the pie grows. My argument is that the slices get thinner for everyone except the foundation model layer. Both can be true at once. What’s changing isn’t whether software is a good business. It’s the shape of the companies that win. More of them, addressing more problems, each commanding less per seat than the last generation did. A fatter, flatter distribution of winners.

That’s not a worse world for software. It’s a different one. But it’s a meaningfully worse world for a specific kind of company: the overcapitalized one priced for the last generation’s multiples.

Over the past decade as a founder and early stage employee, I’ve learned to love capital-efficient businesses. But now feels like the moment to be almost religious about it. If you raise a lot of money and spend into an ACV assumption that turns out to be 40% too high, you don’t get a do-over. If you’re not in the right part of the Buy Window post-AI, having more runway just means having more time to discover you’re in the wrong business.

The companies that will look smart in five years are the ones that kept their burn low enough to figure out where they actually sit before committing to it. That’s true for founders, and it’s true for the funds backing them.

That’s not a reason not to build. It’s a reason to be thoughtful about what you build, and severe about how much you spend to find out.

The upper half of the chart — deep workflows, vertical or horizontal — is where I’d spend my time. Depth creates the kind of stickiness that resists both incumbents and vibe-coders.

More software will be built than ever before. Less of it will be bought.

Edwaert Collier, Vanitas Still Life, ca. 1662. A reminder that the Buy Window has always been narrower than it looked.