Unicorn Lists Are Prediction Markets. This List Is a Scorecard.

Most people in the startup ecosystem are focused on the future. What trends and new technologies will matter? Which founders will define the next decade? Will a startup become a unicorn, decacorn, or an episode of the Acquired podcast?

We were curious about something else: what does success actually look like after the deal closes and the returns are realized?

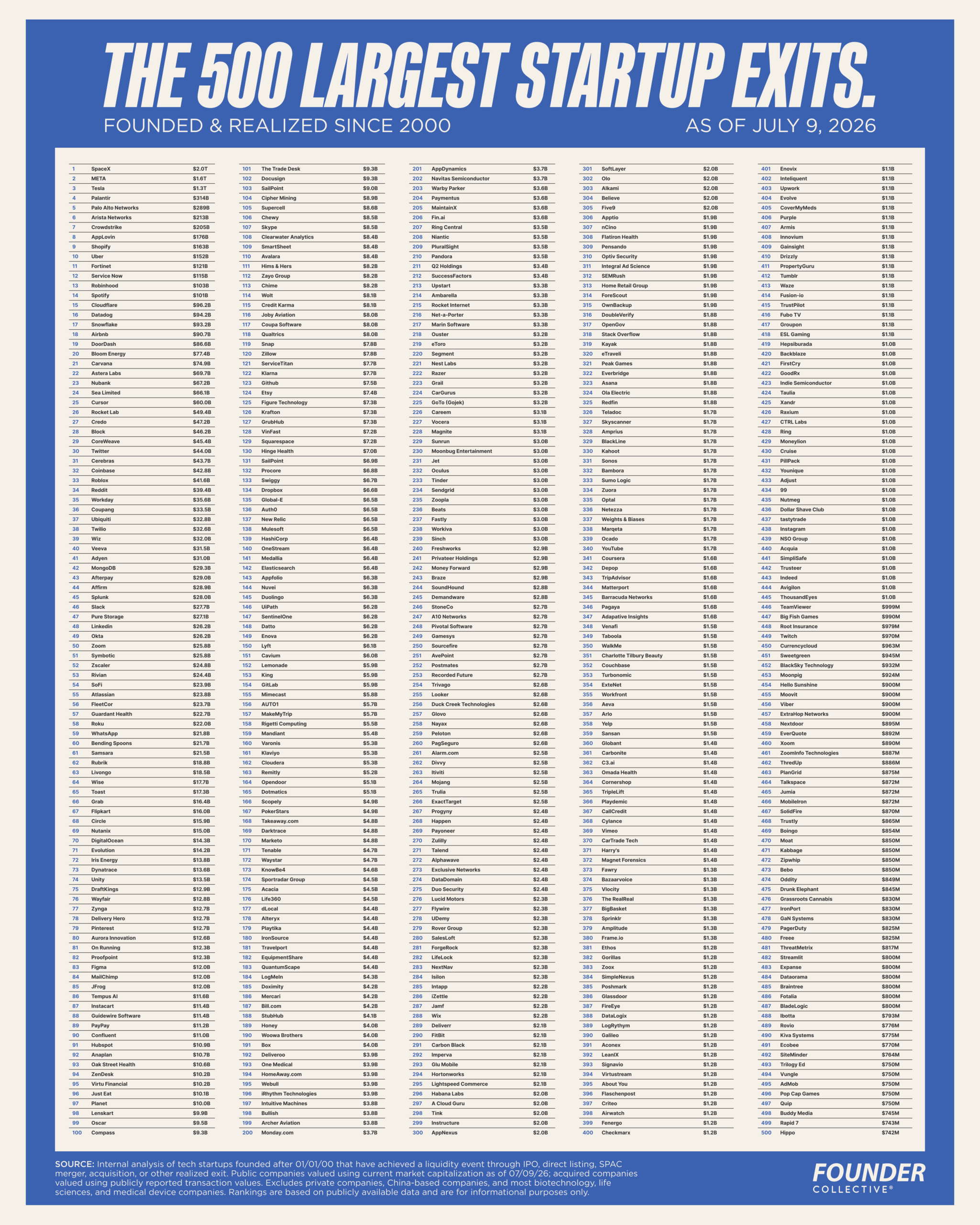

To find out, we assembled a list of the 500 most valuable startup exits, drawn from companies founded since 2000. Roughly 100,000 venture-backed startups were created during that period, so this list represents the top half percent.

We aren’t claiming the game is over, but we are now a quarter century into the millennium. An investor who began their career in 2000 could plausibly be approaching retirement today.

Enough time has passed to look beyond forecasts and fundraising rounds and ask what the last quarter century actually produced. VCs complain of the lack of feedback loops, so we’re looking for the best proxies.

Unlike markups and paper valuations, DPI doesn’t lie.

Initial Findings

There are a few top-line observations worth noting.

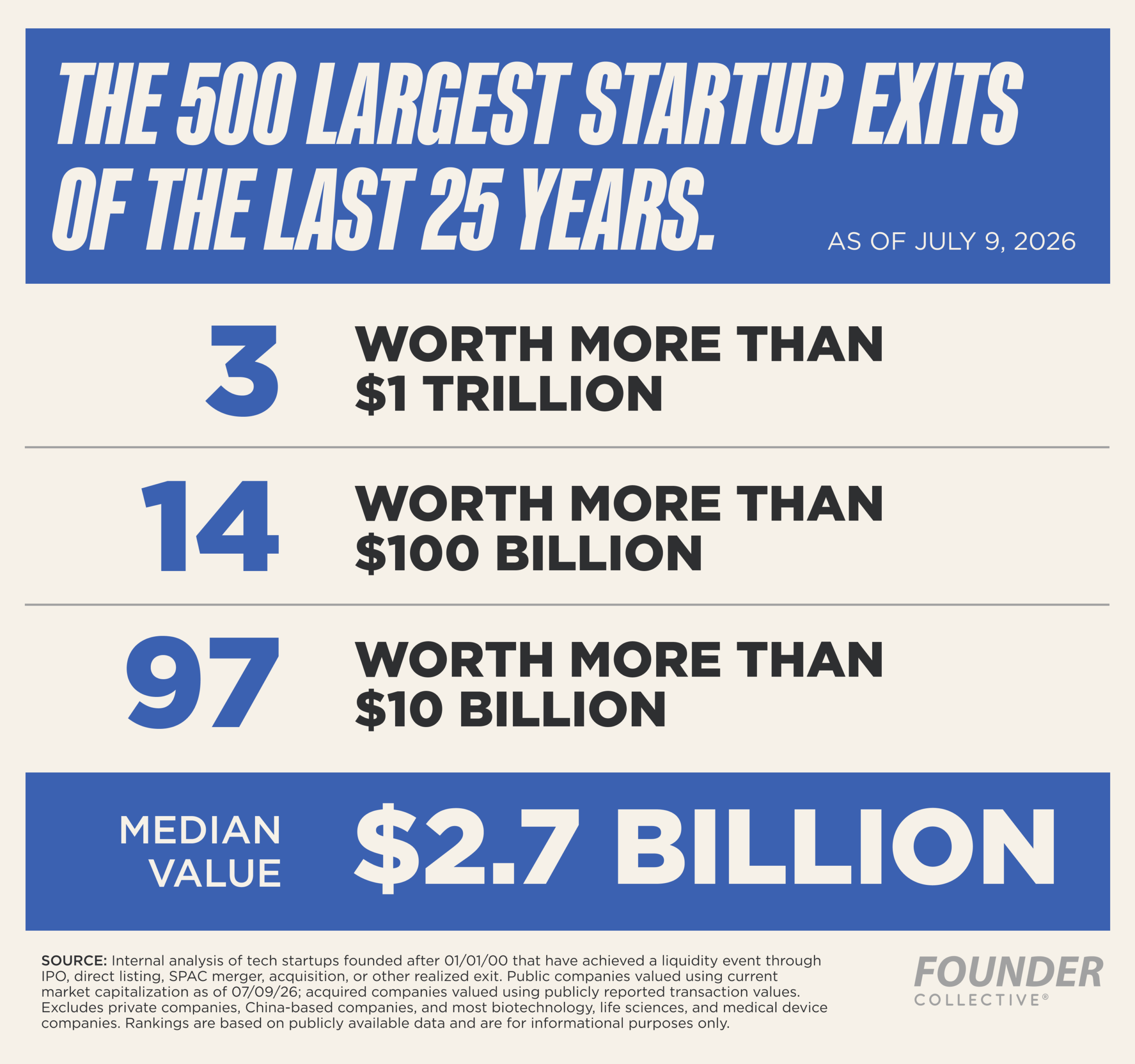

- $10T in value has been realized across the startup ecosystem over the last quarter-century.

- The median value is $2.7 billion.

- Three startups are worth more than $1 trillion.

- Around a dozen are worth more than $100 billion.

- Fewer than 100 are worth more than $10 billion.

- Roughly 50, or 10%, are worth less than a billion dollars.

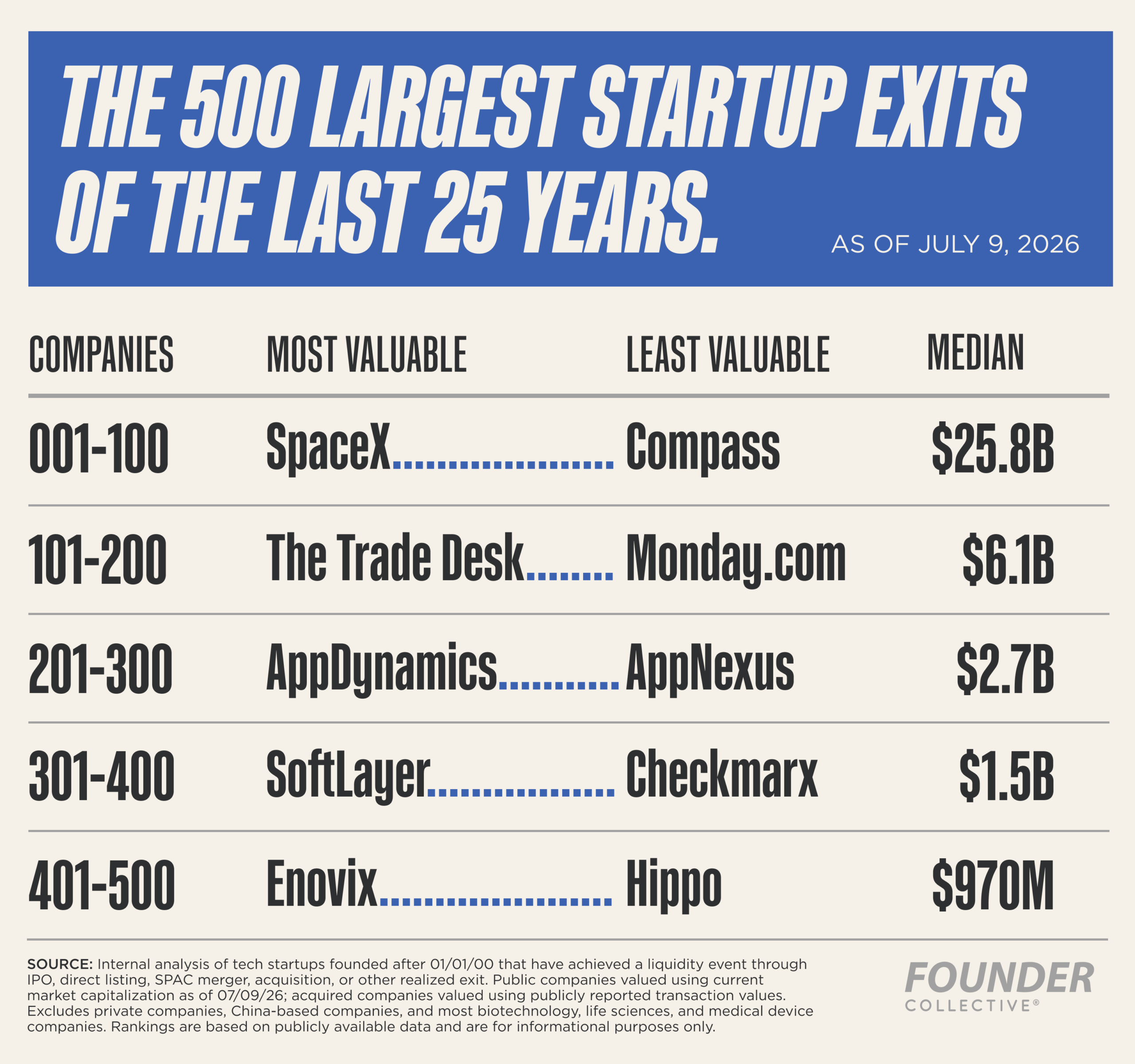

The top company on this list, SpaceX, is worth $2 trillion. The 500th spot is Hippo at $742 million. Again, the median is $2.7 billion.

That median figure was the most surprising.

It represents roughly the top 0.25% of all startup outcomes from the last 25 years. Even so, there are now corners of venture capital where owning 20% of a company that exits for $2.7 billion does not return the fund. Among some entrepreneurs, a $2.7 billion round, not a $2.7 billion exit, is viewed as the true mark of outsize success.

Understanding these numbers is important, or “load-bearing,” as the AIs might say, for founders and investors alike.

VCs often justify high entry prices with a simple argument: if you’re in the next Uber, it doesn’t matter what you paid. That’s true. It also describes roughly one company every couple of years.

Founders, meanwhile, fixate on crossing the billion-dollar threshold as quickly as possible, while ~10% of the 500 most valuable startup exits of the modern era did not.

Past performance is not indicative of future results. But if startup outcomes continue to resemble anything like this distribution, many founders and investors may be benchmarking themselves against overly ambitious assumptions.

Of course, this is an inherently backward-looking exercise. Some of the defining companies of the current generation—OpenAI, Anthropic, Stripe, Databricks, and others—remain private, and trillions of dollars of value have yet to be realized. The rankings will change as liquidity events occur, but what if the broad pattern persists?

Twenty-five years into the modern startup era, we finally have enough data to study realized outcomes rather than anticipated ones. Unicorn lists are a market of expectations. This list is a ledger of results. Plan accordingly!

Methodology: What’s included in this data?

Exits, not estimates: Lists of unicorns are useful, but they are only forecasts. Our focus is outcomes. Every company on this list has returned capital to founders, employees, and investors.

Post-dot-com-bust only: We focused on companies founded after January 1, 2000. In addition to being a nice, clean starting date, it also tracks with the Dot-Com bust. This sample excludes five of the “Magnificent Seven,” but we are trying to understand the modern startup era, not companies that were founded when Jimmy Carter was president or Napster was a going concern.

Software and software-adjacent companies: We excluded most biotech, life sciences, and medical device companies from this list. This is an entirely subjective decision, but we wanted to create a list of the kind of companies that our peers and we might have invested in. While they do important work, we have little overlap with innovators pursuing novel gene therapies or cutting-edge surgical devices.

So why is SpaceX on the list? Because it was founded by Elon Musk. Why is CoreWeave in the data when other semiconductor companies aren’t? They were backed by investors who largely invest in the software ecosystem.

The boundaries are admittedly fuzzy, but we generally focused on businesses whose value was created by software, by people with strong ties to the software ecosystem, or those who raised capital from VC firms that primarily invest in software. If you think a company was unfairly omitted, please let us know.

Everything but China: China is one of the world’s great technology ecosystems, but it has historically been less accessible to foreign venture investors than the U.S., Europe, LatAm, and other parts of Asia. If someone wants to analyze the Chinese startup ecosystem, we’d genuinely love to read it, but it is outside the scope of this project.

Current pricing: Public companies are valued at their current market capitalization, not their IPO or peak valuations. We’re writing this analysis based on data as of July 9th, 2026, but all figures are subject to change due to fluctuations of the stock market.