Unicorn Lists Are Prediction Markets. This List Is a Scorecard.

What does success actually look like after the deal closes? Unlike paper valuations, DPI doesn’t lie.

Description text goes here. Description text goes here. Description text goes here. Description text goes here.

What does success actually look like after the deal closes? Unlike paper valuations, DPI doesn’t lie.

My own colleagues ask me this all the time. So I went through my whole portfolio, more than 75 companies over a dozen-plus years, and looked as hard as I could.

Mass production is faster, cheaper, and often “good enough,” which is why it caps you at average.

The world holds more randomness than we admit. Default Yes to showing up.

You’re a different company at each round, so pitching the same story means pitching the wrong one.

The strongest founding teams are like the two wheels of a bicycle. One wheel provides power, the other direction.

Strategy matters, but it can become a substitute for the unglamorous work of finding the next great company.

Token spend is a new line item every company has, and no one can tell you what it’s buying.

The feedback used to hit immediately and I carried it home every night. As a VC I can be wrong for a decade before I find out.

The right founder clears regulatory hurdles that take outsiders years to copy, and owns the category while they catch up.

We’re trained to source, evaluate, and back, but not how to make a one-way valuation call on a private company with the window closing.

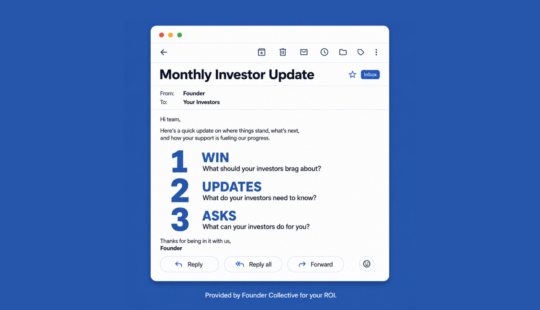

One win, two updates, three asks. Make it easy for us to help, and we will.

In hedge funds, your performance is marked daily. In venture? It’s much murkier.

You just need to spend where your budget reads as authority.

The same stats could describe radically different companies now, so the labels tell you almost nothing about the risk profile.

Raising lean assumes you can predict what the next round rewards. Lately, that’s gotten very hard to call.

The best hardware companies now run like software businesses with a physical wedge into your home.

It works like a venture portfolio. Make enough careful bets, and the odds compound in your favor over time.

Picking well used to be the job. Now, GPs who can’t build an organization are in trouble.

You can’t engineer serendipity, but you can keep showing up for it.

As AI commoditizes models and infrastructure, defensibility is shifting to taste, workflow, and trust.

Resistance to AI runs on emotion, not aesthetics.

The best founders watch faces, not dashboards.

Conviction isn’t the urge to catch up with the room, it’s belief in a founder’s decade-long vision.

So much of VC is the thinking process, not the research.

We’re good at spotting AI’s obvious tells. But the greater risk may be subtler, in that we’re outsourcing the connective tissue of thought itself.

A curated reading list from the most interesting founders, operators, and investors in NYC and beyond.

The algorithm of being a good VC and the algorithm of being a good human and friend are basically the same thing.

In defense of conviction over consensus.

The founder alone carries a responsibility that cannot be delegated.

Is the confusion a bug or a feature right now — or just the cost of doing business?

If you’re considering starting a company, beware the ‘shotgun wedding.’

When I zoom out, I see seed VC evolving in generations.

More software will be built than ever before. Less of it will be bought.

The information environment is pushing everyone toward the same conclusions at the same time.

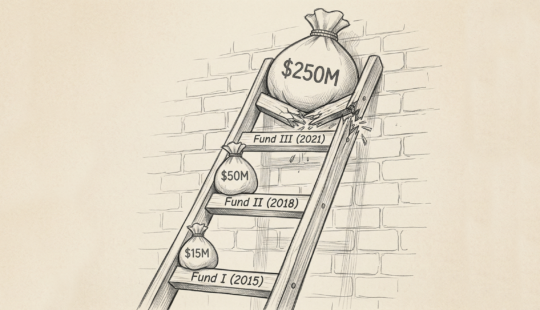

The same check into the same exit returns a third of what it did in 2012, so the answer matters.

I used to wonder why there is so much transition in venture. I think I understand it a little better now.

Most startup problems come down to three words founders hesitate to use.

Behind closed doors, co-investors weigh where they sit on reserves before they weigh your metrics.

The strategy that kills more companies than it crowns.

A founder in his late 70s gave me that advice ~20 years ago. This week, he sold his company for $29B.

Even at OpenAI’s scale, you still can’t do everything at once.

The more individualistic digital content becomes, the more we’ll crave IRL engagement that brings together communities.

In venture and product, we’re obsessed with removing friction. But when it comes to developing young adults, friction is the feature.

Why venture capitalists don’t retire (and what it means for founders)

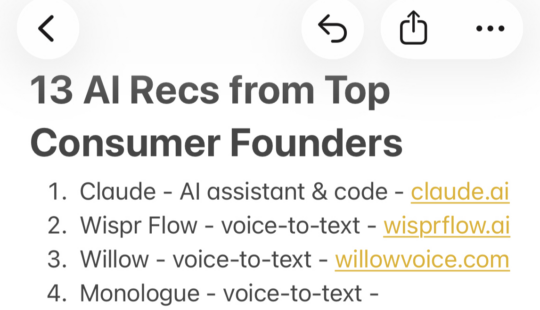

We hosted a forum of top consumer founders in NYC, from a brand launched last month to a company doing 9 figures in revenue. Here’s what they cited as their favorite AI tools right now.

From autonomous workflows to the rise of a new AI-specialist role, here is how artificial intelligence is transforming game development today.

I’ve spent 30+ years building and backing companies, and it’s never felt like quite like this.

The most durable companies are often built by founders who test obsessively, take risks when the timing is right, and embrace the quiet, unglamorous work of building brick by brick.

The case for thinking through it yourself

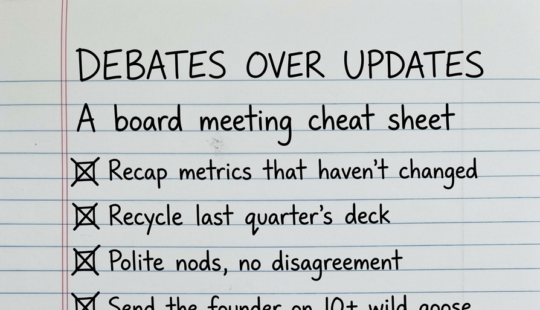

If your next board meeting is approaching, figure out the single most important decision you’re facing. Then structure everything around that.

As a former hardware founder turned VC, I’ve seen the binary risk of building in atoms. Here’s why hardware is the ultimate defensible moat in the AI era.

It’s investing 101, and yet we’re failing as an asset class.

Ignoring the “boring” stuff is where founders create multi-million-dollar unforced errors.

After reviving Founder Breakfasts in Boston, I noticed two big shifts in the city’s startup ecosystem over the past decade.

A founder who’s all over it should have tight answers for all of these and more.

To build an enduring brand, founders must ask themselves over and over: Would this new hire sharpen our compass or dilute it?

Suno just hit $300M ARR. As their sole pre-seed investor, I didn’t have a grand AI thesis.

There’s so much to know and so many ways to know it, and yet it feels harder than ever.

When Jack Altman merged his fund into Benchmark recently, it wasn’t just a partner announcement, it was a sign that change is afoot in this business.

On the difference between conviction and stubbornness

When everyone optimizes for the same signals, non-obvious founders and out-of-favor categories get screened out before the first meeting.

Venture is splitting into two distinct business models.

Tools can generate content. Designers decide what is worth keeping.

There’s a lot of noise right now about $15B funds and $5B rounds. For most founders, that’s a distraction.

Change is inevitable. Chaos is optional.

Psychologists distinguish between two types of smarts: Fluid Intelligence and Crystallized Intelligence.

A portfolio company recently sent us a spreadsheet of 200 investors they wanted introductions to, listed alphabetically. I applaud the comprehensiveness, but the request was ill-formed.

Run the math before you buy the myth.

I sometimes joke that we’re an event-planning firm with a side business in VC.

Pensions funds, SWFs, university endowments, and other large institutional LPs have specific needs. The defining one is scale.

You have to be a tactical animal to survive, so that you can become a strategic leader to win.

A word of warning to founders – if you’re talking to a VC, you are pitching.

Founders are now editors-in-chief of UX, and they must be ruthless curators.

I used to think this job was 90% picking. Now I realize the algorithm is far more complex.

The tragedy is that M&A is a test you only get to take once.

We know the pattern, yet we repeat it because the fear of missing the category-definer outweighs the fear of overpaying.

An investor who never makes you mad won’t help you make money.

I have a few favorite sayings in business, but this is the one I find myself constantly trying to disprove.

If you are a founder staring at a term sheet with a dizzying valuation, I am urging you to do one specific piece of diligence before you sign.

I went back and tagged the founders I’ve backed with a few attributes. The data challenged two of my strongest prior beliefs.

I spent last weekend doing something I’ve wanted to do for years but never quite had the data or time for.

On paper, Apple has all the prerequisites to build the ultimate personal agent, and yet…Apple isn’t a serious AI player. Why?

When you build here, you aren’t just plugging into a “tech scene” – you are plugging into the actual machinery of the world.

The reason AI progress is uneven.

Artistic careers may be more challenging to forge, but making art as a way of seeing, understanding, and social signaling has a bright future ahead.

My outlook for 2026.

On founder-market fit and aptness over novelty.

Venture capital does itself no favors with an all-or-nothing mindset.

In hindsight, the 2009-2015 era looks like a “Golden Vintage.” But looking back with an honest lens, I have to ask: Was it all skill, or was there a massive arbitrage opportunity?

Why I’d never be a solo GP or solo founder.

It’s okay to cope and seethe, but we also need to see clearly.

With the IPO window still creaky and M&A volume unpredictable, the secondary market has exploded into a $200 billion beast.

Why the “idea maze” starts with who, not what.

“Why You?” is always the critical question we ask at Founder Collective, but in overheated markets, it becomes decisive.

One of the clearest frameworks I’ve seen for evaluating early-stage businesses.

When your life-changing exit doesn’t put a dent in your investor’s fund, incentives misalign fast.

SharkNinja CEO Mark Barrocas recently spoke with Founder Collective GP Amanda Herson at Collective Future.

The interesting value creation is almost always happening in the corners.

I’m skeptical of many startup “rules.” But trusting in exceptional founders has rarely led me too far astray.

It’s part update, part reflection, part board meeting for our own business.

Do VCs improperly index on outliers?

AI systems don’t fail because they’re dumb, they fail because we never define “good.”

In venture, so much happens in the in-between.

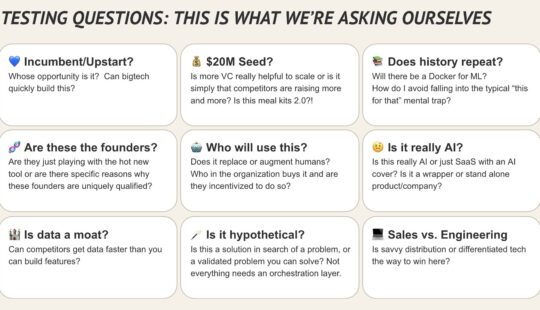

The topic was on evals, something that’s come up again and again in conversations with founders building AI products lately.

Startups are short chapters, but they leave lifelong imprints.

Collective Future reflects a simple belief: that Boston’s next century of breakthroughs will depend less on any single idea and more on our ability to communicate and develop them together.

From presidential biographies to cyberpunk classics, from the history of the microchip to the art of hospitality, each book on this list was handpicked by one of New England’s foremost decisionmakers.

The three levers for steering pre-trained models and the evals that guide them.

Having had the pleasure to work with Noah for two decades, I want to share a few reflections.

When answers replace clicks, publishers, brands, and platforms face a new incentive structure.

Every week I see pitches that follow a similar pattern: “X for Y, powered by AI.” I call this promptware.

How Big Tech is gutting AI startups without actually buying them.

Why technical leadership just got exponentially harder.

On the social cost of thinking out loud.

Get real-time advice from the Founder Collective partner – whether you need a gut check, strategic input, or just someone who’s been there. Powered by Regal AI.

One of my editors at Wired used to say, “Put a fact in every sentence.” It was a way of eliminating throat-clearing intros and excess opinion. In our era of ghostwritten gray goo, my key element of style is this: put a piece of you in every sentence.

If a line doesn’t contain your DNA, delete it.

We’re proud to share that Eric Paley, our long-time partner and dear friend, has been appointed Secretary of Economic Development for the Commonwealth of Massachusetts by Governor Maura Healy.

Eric has chosen to step away from Founder Collective to assume the role of Secretary of Economic Development for the Commonwealth of Massachusetts. Anyone who has ever met Eric will instantly know why he is an inspired choice and a perfect fit.

Why product > perfection and business outcomes > abstractions.

If you believe AGI is close, how do you justify backing a startup with a 5–10 year horizon? It’s a fair challenge, and one that deserves a better answer than: “We believe in founders.”

As one LP told me, “You’re going to be wrong for selling too early or wrong for not selling – either way you’ll be wrong.”

How do ambitious founder-parents keep it together when life throws pacifiers and pitch decks at the same time?

Apple’s Illusion of Thinking reminds us that transformers may asymptote to human ability and that may be enough to transform the world.

At Collective Future, Red Antler’s JB Osborne explained why vibes are the key to ROI in the age of AI.

Myth Model Takers, Not Model Makers: The Reality of Modern AI Work

The career ladder is breaking. The new edge: critical thinking, systems fluency, second-order reasoning, and the ability to orchestrate.

Your internship isn’t just about completing tasks, it’s your chance to see how things actually work inside an organization.

Board meetings steal hours from your calendar. If you’re not getting sharper, you’re just burning time.

You no longer need a fleet of middle managers to build something big, just a small team

Things I overheard in conversation with a $50B product leader and the head of product at the hottest AI product company around.

Founders never rested, now no one does

The rarest skill isn’t building fast anymore—it’s knowing what’s worth building.

Venturing in Public — 4/30/25

Minting Money in the Foundation Model Gold Rush

For the last decade, the “endless aisle” was the mantra of every omnichannel retailer — infinite options, ultimate convenience, and unlimited scroll. But choice is no longer empowering. It’s paralyzing.

You can’t build 10x software with 1x interfaces

What AI remembers, what it forgets—and what never makes it into training

Venture capital has bounced back from 2021, but the competition to get into the hottest companies has continued to drive valuations to extreme heights.

Why tool use is getting commoditized—and what still counts as a moat in the age of MCP.

Venturing in Public 3/26/25

Venturing in Public – 3/20/25

In looking at the portfolio recently, I was surprised to see that our DTC portfolio – ranging from baby toys to cat food, furniture, skin care, and more – will do over a billion dollars in sales this year. A billion in sales!

Think of each funding round as part of an ongoing strategy—a multi-stage game, where every decision has ripple effects on the long-term trajectory.

We’re thrilled to announce that Jack Arenas has joined Founder Collective as the new Principal in our SoHo office. He represents the value and ethos of FC – he’s a builder at heart, lived the ups and downs of the founder journey and loves to work with founders across the tech industry.

After a decade of building and scaling startups, I’m excited to embark on my next chapter as a Principal at Founder Collective in their NYC office.

VCs are famous for asking startups, “What is stopping Apple, Meta, and Alphabet from doing this?”

Pivots are part of many successful startup stories, but there’s no clear playbook on how to make them work. There should be no shame in pivoting, despite what many founders think, but they need to be well thought out before burning the boats.

When I started in VC, there was one incentive — capitalize startups, help founders build their businesses, and bring in additional capital (when necessary). Hopefully, if the stars aligned, the funds delivered outsized financial returns for the risk, ideally 3X or more, to their LPs. This model was a relatively well-tested formula for venture-backed startups — provide enough capital to the company (but not too much) and maximize its chances for a healthy return, hopefully in less than ten years.

AI is going to change everything. At least, that’s what everyone in Startup-land believes.

Fifteen years into my venture capital career, I’ve come to believe there are two undeniable laws of startup physics: 1) Capital compounds both positive and negative formulas. 2) All positive formulas compound at diminishing rates of return.

Staying true to our roots with a new Fund

If you work in tech or have attended a conference over the last ten years, you’ve likely come across S’well water bottles. Sarah Kauss, an accountant turned entrepreneur, invented the iconic, insulated vacuum flask as a sustainable and stylish alternative to single-use plastic water bottles. Sarah launched the product in 2010 with $30,000 in savings and grew the company to over $100 million in revenue annually while turning hydration into a form of sustainable haute couture. And she did it without a drop of venture capital.

I couldn’t be more excited about joining the partnership at Founder Collective. The last two years on the team have been energizing, and I am even more bullish about the next 20.

VCs offer a lot of advice from a 30,000-foot view. Here are 7 bits of practical wisdom I gleaned when managing a large, resource-constrained, growing team that you can apply to your startup today.

Being a successful venture capitalist requires various skills, but we believe that the ability to empathize with founders separates the good from the great. The first years of a startup are a rollercoaster of stress for founders where success is unpredictable and sometimes seems out of reach. Most investors have no idea what operating under that level of ambiguity is like, but Amanda Herson does.

As capital gets scarce, I want to relay a few thoughts on startup marketing that Kayak founder Steve Hafner recently shared with the Founder Collective portfolio.

The next year will be challenging for startups. Promising companies will struggle. Many will fail. The only consolation is that the “era of indifferent capital” is coming to a close — may it never return.

Does raising a large amount of capital make a startup more likely to succeed? Is capital a weapon? Do startup founders need to “go big or go home?”

An unrepresentative, statistically insignificant, but still interesting peek at the current M&A market

Entrepreneurs are often so fixated on “getting to yes” with a VC — and will go to great lengths to answer any question posed to do so — that they forget to ask the VC any questions.

There’s never been a better time to build a company outside the Bay Area

You can put off monetization, but not thinking about monetization

Many “atypical” markets are surprisingly M&A friendly, but VCs may not recognize the potential buyers without guidance

As entrepreneurship has professionalized, jargon has proliferated, and platitudes pervade pitches. One helpful tool to combat this scourge of short-hand is:

🏕️ “The Summer Camp Test” ⛺️

I recently tweeted about the importance of financial models in evaluating seed-stage pitches

A high-quality startup problem is when the company starts to scale but one of the co-founders can’t grow at the same pace as the other. It’s a good problem but a real challenge nonetheless. Here are some thoughts on how I’ve seen it handled well (and not).

I’ve had the good fortune to be an investor for almost 15 years and have backed 100s of startups. Only one company in all that time deliberately defrauded its VCs.

Even for strong startups, fundraising is a marathon that requires near constant attention for 8–12 weeks. The process is punishing, and riskier than you might imagine. You need to prep for it as seriously as you would a race.

One of the secrets of B2B entrepreneurship is that a good enough product with exceptional distribution will win more often than an exceptional product with mediocre distribution.

When getting ready to pitch VCs, founders often jump right into assembling a slide deck. I think this is a mistake. I’d suggest that you start by writing twenty headlines that sum up your startup, and only then build the slides.

One argument I hear in favor of big $$$ fundraising is that it will help in recruiting. It’s a logical enough belief but mistaken. It assumes there’s a linear relationship between the amount of funding raised and caliber of recruits.

I have the great privilege of seeing a lot of startup pitch decks and have noticed a few common narrative patterns that are counterproductive for otherwise interesting companies. If you’re getting ready to pitch a VC, try to avoid these traps.

If you’re pitching investors, one of the easiest ways to improve your deck is swapping out blank interstitial slides, or the dull logo cover slide, with pictures of your product in use or in context.

In my role at a VC firm, I have the privilege of seeing the pitch decks of startups as they set out to raise new funding. In the main, they’re masterful, but I’ve seen a lot of founders making a similar mistake—including quotes from random users in their presentations.

These are the liquidity events that give the impression that startups are a great way to “get rich quick,” even though building a saleable company often takes the better part of a decade. Less often discussed, or championed, is a third option — the “get rich slow” method of building a company and making millions of dollars in profits, for years or decades.

The “Series A crunch” sometimes still feels real. It dooms many startups that could otherwise have easily survived if they had been more strategic about their seed-stage fundraising.

In a world where IPOs are an unlikely outcome and traditional M&A exits are difficult to manufacture, there is a new alternative for liquidity starved founders and investors — The PE exit. It’s an invisible ecosystem to most, but when you see a headline about a PE firm making an “investment” in a mature SaaS startup, and there is no mention of valuation, or even what series it represents, you’re most likely witnessing an acquisition, of sorts.

How do you become humongous with humble financing? There are a few principles that seem common.

In 2007, Groupon took in the first million dollars of what would ultimately be $1.4B of venture capital, raised with ambitions of reshaping shopping. For a while, it looked like group buying, social commerce, daily deals, or whatever you call the practice of time-limited sales paired with social pressure was really going to change buying behaviors in a big way. In the space of four years the category exploded:

There’s a widespread belief among founders that venture capital is a precursor to success. It is true that VC is a common denominator of the most successful tech startups, but it isn’t a prerequisite, especially at the early stages.

There’s no good way to tell your board that you’ve blown a quarter, or your superstar head of data science is jumping ship to Google. Still, breaking bad news is a key skill for founders and delivering it well is often what keeps a company alive.

When I used to write for Wired, a cold email was the lowest probability way to get press, but it still worked with some regularity. Cold emailing a VC is a similarly low-percentage play, and many of the best VCs in the world advise against the practice. Still, it does work from time to time.

In my role at a venture capital firm I have the good fortune to see a few dozen pitch decks a month. Some are brilliant, and others require more time to bake, but almost all of them waste the first slide.

For some entrepreneurs, raising capital is effortless. When you see a company raise tens of millions of dollars, series after series, especially if they have few other milestones to promote, you know you’re in the presence of a world class presenter. Fundraising is a startup super power, just like consumer product instincts and B2B sales acumen. Some founders are just “natural athletes” who possess a knack for storytelling paired and charisma, typically topped off with some credibility in a prior venture.

David Pierce has written an excellent post-mortem recording the last days of a hardware startup called Doppler Labs. The post carefully details all the challenges in launching a consumer product, and Doppler Labs co-founder Noah Kraft provides a colorful summary of the experience:

There’s a lot of good advice on writing investor updates, but one of our portfolio CEOs recently wrote an update that was so good that I thought it could serve as a template for entrepreneurs everywhere. It’s B2B focused and largely positive in tone, but it’s easy enough to copy, paste, and customize for B2C startups or less upbeat news. Just swap out the [bold] content and you can keep your investors in the loop with almost no effort.

“I need to find a industry or product I’m passionate about.” I often hear this from entrepreneurs and it frequently means wanting to start a business in a consumer space that they love—music or gaming, for example. It’s an understandable impulse. If you’re going to start a business that will consume your life for years, why not make it something you’re interested in?

Imagine you’ve spent years working on a startup with the hope and a credible plan to build a billion dollar business and along the way get an offer for $100M? You still believe in your vision, but a nine-figure sale would represent a rich premium based on your traction and early revenue growth. Should you take it?

Hundreds of millions of people use Firebase-powered apps every day, though they may not realize it. The company started as backend-as-a-service for app developers that made real-time functionality simple for Shazam, NPR, SeatGeek, and hundreds of thousands of other services.

One of the questions a VC gets most often is “what are you interested in?” Many investors have developed “themes” that become a shorthand used to discuss the types of deals they like

Do companies that load up on venture capital actually outperform those that more efficiently deploy capital? We looked at 71 tech IPOs from the last five years to find out.

Capital has no insights. Don’t trade a solid business for a lottery ticket.

We’ve been trained by infomercials that “But wait, there’s more!” is a powerful sales pitch. Not surprisingly, this approach is used frequently by entrepreneurs pitching their startups. Somewhere between slides 12 and 15, the passionate founders take a breath, clear their throats and declare “But the real opportunity in this business is …”

Getting courted by investors is an exciting milestone for any start-up. But when the VCs start calling, don’t let their enthusiasm cloud your judgment.